Your ERP Has a Hidden AI Problem, and It's Growing Every Day

AI Integration Debt: what it is, why ERP is especially exposed, and why your org's AI readiness score doesn't tell you what you think it does

Your ERP Has a Hidden AI Problem, and It’s Growing Every Day

AI Integration Debt: what it is, why ERP is especially exposed, and why your org’s AI readiness score doesn’t tell you what you think it does

I’ve spent more than twenty years inside ERP systems in general and Oracle JD Edwards environments in particular. I’ve seen a lot of things getting bolted onto ERP systems without enough thought given to what happens next. However, this time unlike other integrations, AI integration feels very different.

What’s happening right now with AI integrations in enterprise ERP is not like previous waves of technology adoption. The stakes are of course higher, the timeline is compressed, and the failure mode is invisible until it’s expensive. I’ve been trying to name it precisely, because I think sloppy naming is part of why organizations aren’t taking it seriously enough.

Here’s what I am calling it: AI Integration Debt.

Every enterprise technology leader I talk to these days is under the same pressure right now: get AI integrated into the business, fast. It is pretty much the same pattern all across on how it manifests. The board wants it. The CFO is asking about ROI. The vendors are promising transformations. And the projects are excited about it, given all the hype all around.

So teams move quickly. They connect an LLM here, a predictive analytics service there. They build a workflow automation using Azure AI. They wire it into the ERP through an API call, develop orchestrations, leverage MCPs, fiddle with agents, but in the end document it loosely, and ship it before the quarter ends.

Six months later, that AI service has already released three updates. The API contract has changed shape. The original developer who built the integration has moved to another team or possibly to another organization. The model behaves differently with new data patterns. And somewhere in the ERP landscape, a procurement workflow is silently producing outputs no one fully trusts anymore.

Nobody called this a failure. Nothing really broke. There was no incident logged. No alert fired. The system is technically running and the order of business is being conducted without any perceivable hiccup. But something has gone wrong in a way that will take months to surface and possibly much longer to fix.

Little do we all realize, that is AI Integration Debt accumulating in real time.

What Is AI Integration Debt

Technical debt is a concept most engineers are familiar with. Ward Cunningham coined the metaphor in 1992 to describe the accumulated cost of taking shortcuts in software development that make future work harder. Google researchers extended it to machine learning systems about a decade ago, naming the hidden costs that pile up when ML systems are built without enough care for long-term maintenance.

AI Integration Debt sits one layer beyond that. It’s the accumulated maintenance burden, reliability degradation, and governance risk that builds up when AI services get wired into ERP workflows without the architectural discipline, documentation, and change governance that the criticality of those workflows actually demands.

The specific word I want you to hold onto is accumulated. This is not a system crash. It’s not a failed migration you can point to with a root cause analysis. It builds quietly, integration by integration, quarter by quarter, until you have a portfolio of AI dependencies you can’t fully inventory, can’t fully describe, can’t confidently audit, and can’t easily update without risk.

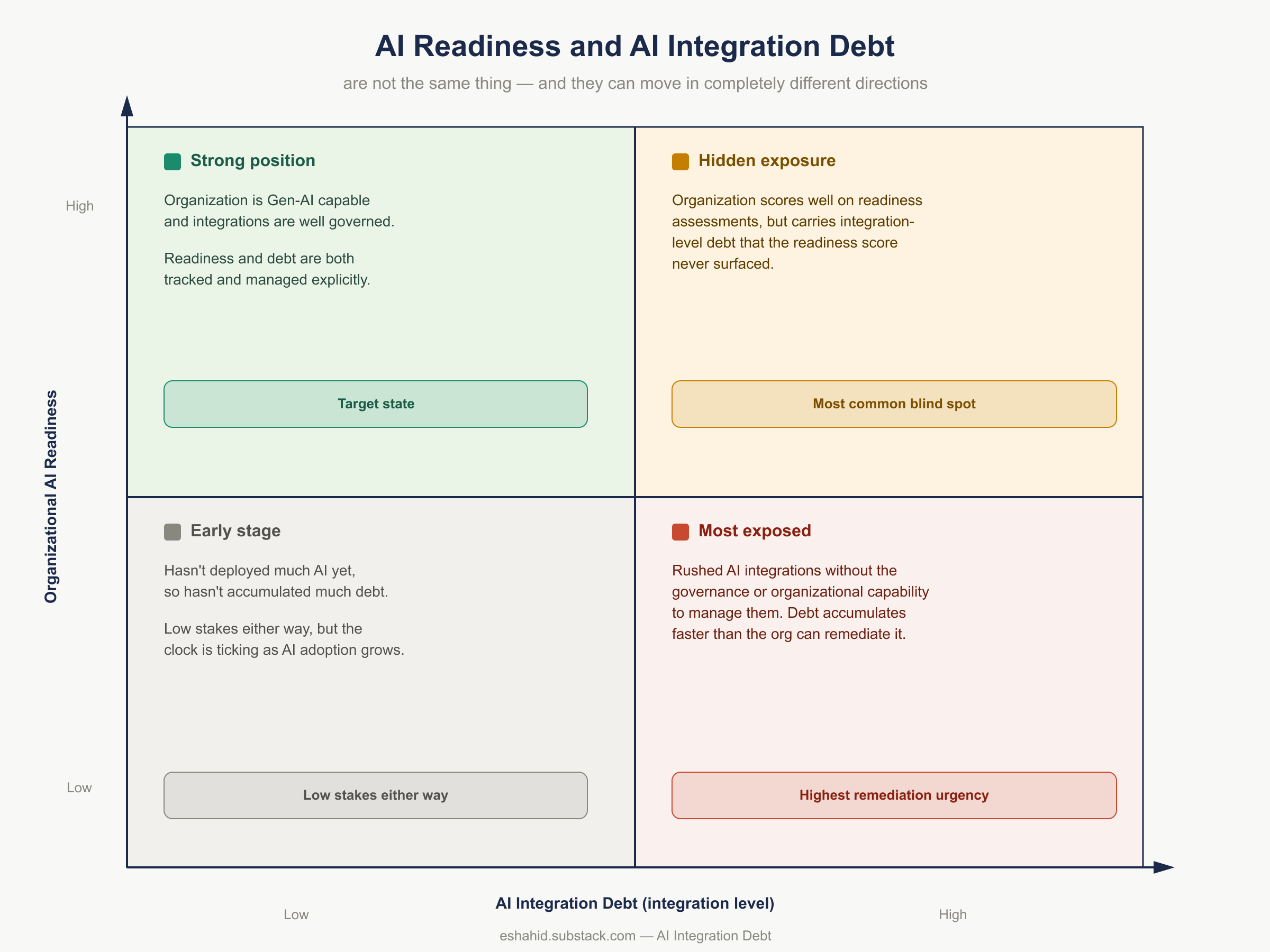

Before I go any further, I want to address something I see conflated constantly in enterprise AI discussions. It is an important distinction to note. AI Integration Debt is not the same thing as your organization’s AI readiness score.

Your readiness score tells you whether your organization has the capabilities to adopt AI well: the skilled people, the governed data, the mature CI/CD pipelines. Those matter. But they describe your organization’s capacity. AI Integration Debt on the other hand, describes the obligations that have accumulated around specific AI components already embedded in specific processes.

These two things can move in completely different directions and often times they do. A highly AI-ready organization can have one badly governed payment-approval workflow carrying severe integration debt. A low-readiness organization that has barely deployed any AI may carry almost no debt simply because there isn’t much to carry yet.

Organizational AI readiness and AI Integration Debt are independent. A strong readiness score tells you nothing about the debt carried by a specific ERP integration.

Your enterprise Gen-AI readiness score tells you nothing about the state of your ERP procure-to-pay workflow that was augmented with AI. That’s a different question. That different question is the thread I am pulling on in this piece.

Why ERP Is a Particularly Hard Case

Most enterprise AI debt discussions focus on standalone machine learning systems or customer-facing applications. ERP is different, and in some ways much harder to get right.

ERP systems are the operational spine of the enterprise. The system of records. In an ERP environment, the system touches procurement, manufacturing, finance, supply chain, and distribution, often at the same time. When AI gets integrated into that environment, the integration is not just a technical dependency. It is a business process dependency. A malfunctioning AI integration in a general ledger classification workflow does not produce a bad prediction that a data scientist can investigate. It produces a misclassified journal entry that your auditors find three months later.

Four things make ERP environments especially vulnerable to this kind of debt.

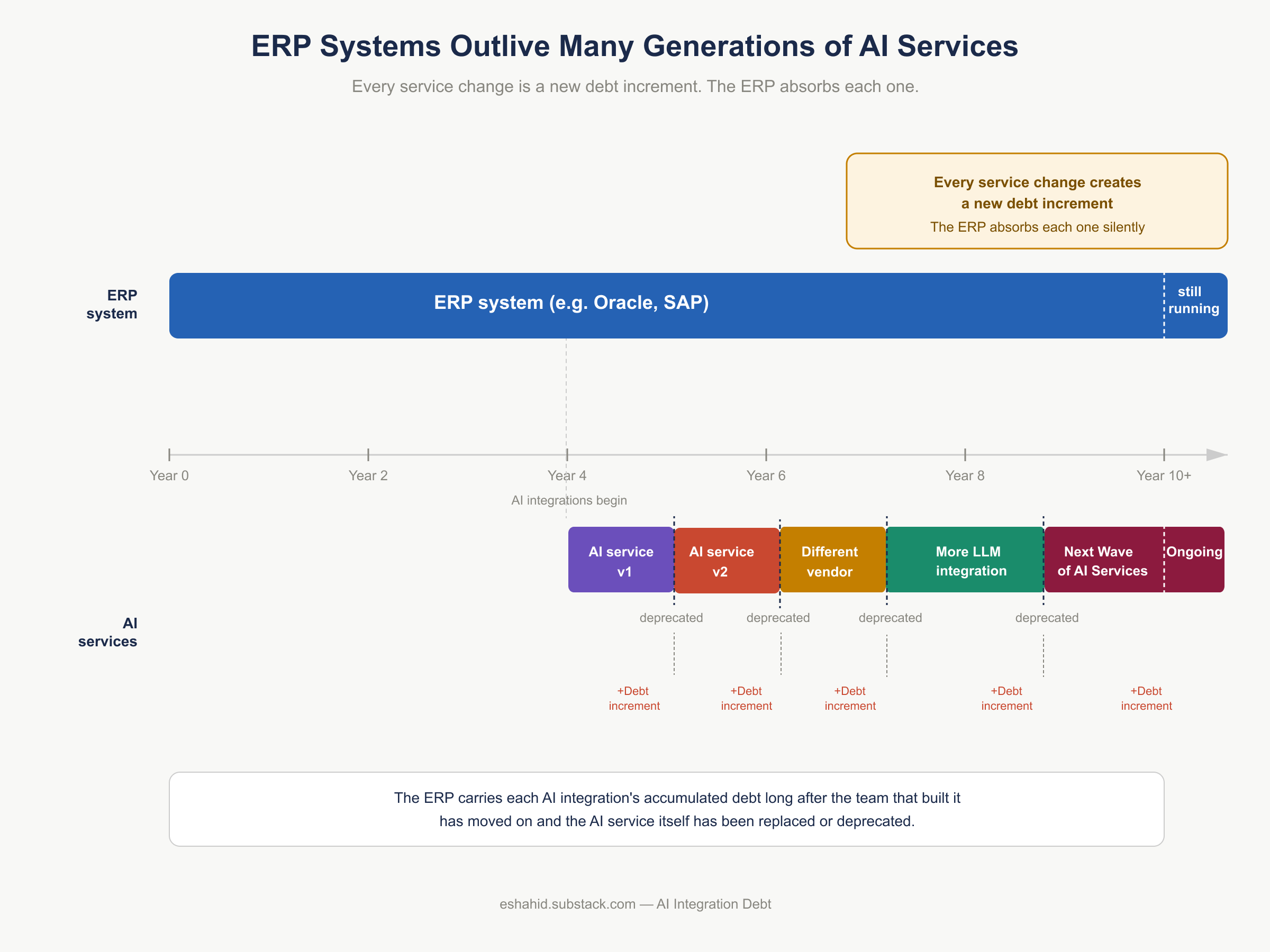

Longevity. Enterprise ERP systems don’t get replaced every few years. They run for decades. An AI integration built for today’s model capabilities has to survive through multiple generations of AI evolution. Every model update, every API deprecation, every shift in how a vendor prices or structures their service creates a new debt increment. The ERP stays. The AI ecosystem around it keeps changing.

Deep process coupling. In most ERP environments, integrations aren’t peripheral features. They are embedded in financial, procurement, manufacturing, and supply chain workflows where a failure doesn’t degrade a user experience; it generates an incorrect transaction. A loosely documented AI integration sitting inside a payment authorization workflow isn’t a technical debt problem. It’s a financial controls problem.

Customization. ERP platforms carry years of organization-specific customization. Every organization I’ve worked with has bespoke logic layered on top of the base platform. When AI gets layered onto that, the integration has to account not just for the ERP’s documented behavior but for undocumented bespoke logic that may not even have a current owner. Debt compounds with every layer.

Governance frameworks that were designed for a different era. Most organizations have mature change management processes for ERP modifications: formal change requests, testing cycles, rollback plans, audit trails. Almost none of those frameworks were designed with model versioning, drift monitoring, explainability requirements, or AI-specific rollback protocols in mind. That gap is itself a form of debt, and it’s one most organizations don’t see until something goes wrong.

The ERP keeps running while AI services cycle through multiple generations beneath it. Every deprecation is a new debt increment the ERP absorbs silently.

Five Ways It Shows Up

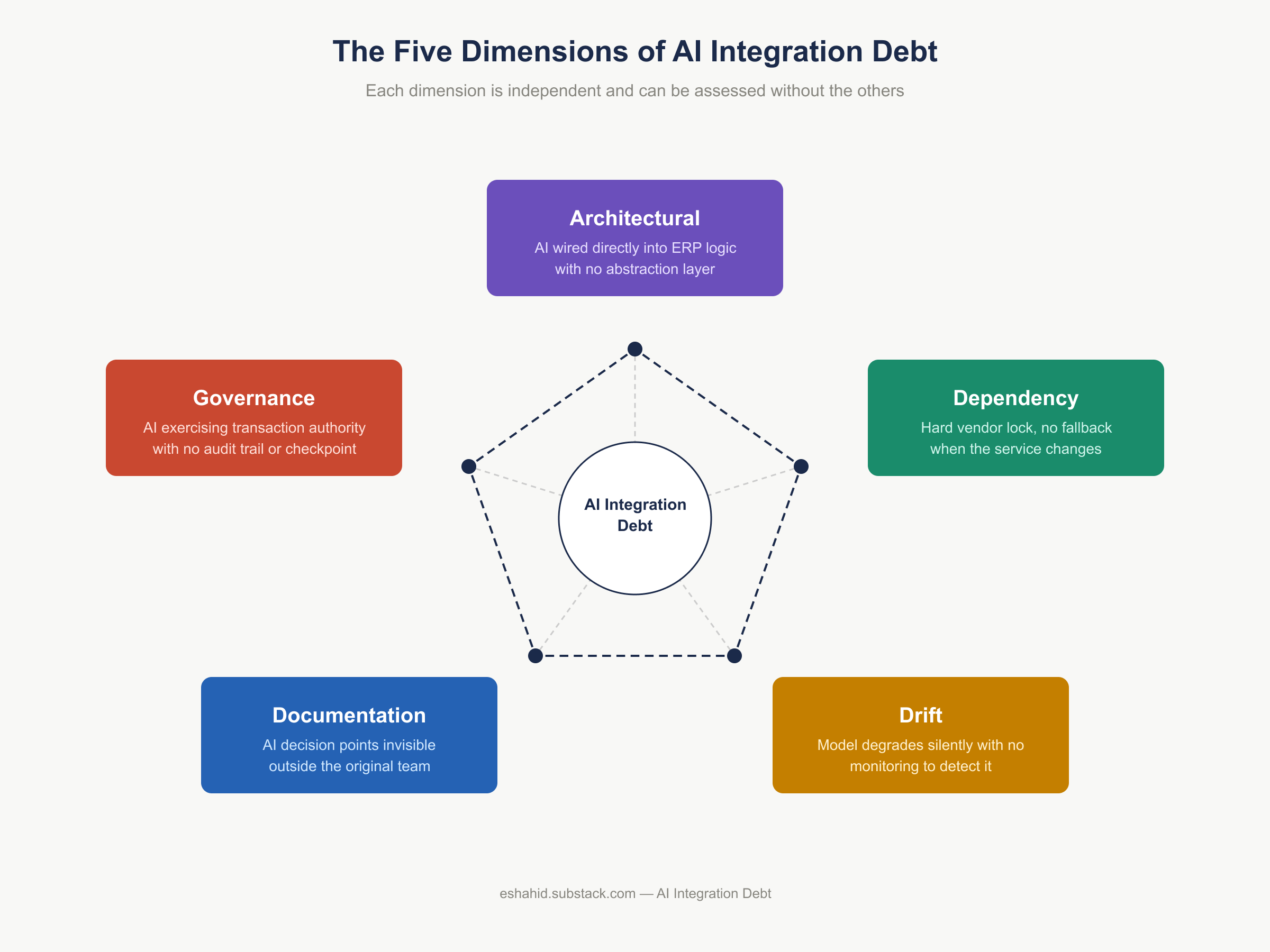

After working through the research and observing the real-world patterns from twenty years in this space, I’ve organized AI Integration Debt into five dimensions.

Each dimension is independent and can be assessed without the others. They also compound. Architectural debt makes governance debt harder to retrofit, and documentation debt makes drift debt more dangerous.

Architectural debt is what happens when an AI service gets embedded directly into ERP business logic with no abstraction layer between them. Direct calls from a business function to an external AI API, no orchestration gateway, tight coupling to a specific vendor’s contract. The practical consequence: when the AI service changes, the business logic has to change with it. And in a heavily customized ERP environment, that change is never as simple as it looks.

Documentation debt is what happens when an integration’s existence, data flow, decision logic, and failure modes aren’t captured anywhere useful. Not in architecture diagrams. Not in runbooks. Not in disaster recovery plans. The debt here isn’t just that the code is undocumented. It’s that an AI-mediated decision point in a business process is invisible to anyone who wasn’t in the room when it was built. When that person leaves, the organization loses the knowledge entirely.

Governance debt is what happens when AI-mediated decision points aren’t subject to the same change-control and audit discipline applied to other ERP modifications. This one matters more in ERP than in almost any other context, because many AI integrations are not merely making recommendations. They are drafting, approving, or executing transactions. An AI component with unbounded transaction authority and no human review checkpoint isn’t a governance gap. It’s a financial controls gap with audit exposure.

Dependency debt is what accumulates from hard dependencies on an external AI service’s specific contract, version, or pricing model. ERP systems are long-lived. AI services evolve rapidly and are deprecated on the vendor’s schedule, not yours. When those two contrasting timelines collide without an abstraction layer to absorb the impact, you get forced rework that you didn’t plan for and can’t defer.

Drift debt is what happens when a model’s predictive behavior degrades relative to a changing business reality, without any monitoring that could detect the degradation. A model calibrated on eighteen months of historical procurement data silently loses accuracy as supplier relationships, SKUs, and process patterns change. You don’t get an alert. You find out when the downstream business process produces results that don’t make sense, usually during a period-end close.

These don’t stay neatly in their lanes. Architectural debt makes governance debt harder to retrofit later. Documentation debt makes drift debt more dangerous because when the model degrades, nobody knows enough about the integration to investigate it properly. They compound each other.

What It Actually Looks Like in Practice

Let me speak from experience and be very specific, because I’ve seen versions of all of these.

The Orphaned Integration. An AI service was integrated twelve months ago by a consultant. The consultant is gone. The integration works, most of the time. Nobody on the current team fully understands how the prompt is constructed, what data is being sent to the model, or what the failure mode looks like. When the AI vendor updates their model, nobody knows how to validate that the integration still behaves correctly. So they assume it does. This is architectural, documentation, and governance debt compounding.

The Authority Void. An AI component is classifying purchase requisitions and routing them for approval. Nobody ever explicitly decided whether this is a recommendation or a decision. The humans downstream started rubber-stamping everything the model suggests, because it’s usually right and there are other things to do. There’s no audit trail of what the model classified and why. There’s no threshold below which the model defers to a human. The AI component has quietly absorbed transaction authority that was never formally granted to it. This is the governance debt pattern that concerns me most in ERP environments specifically.

The Undocumented Dependency. A critical business process depends on an AI service that isn’t in any architecture diagram, isn’t in the disaster recovery plan, and isn’t covered by any SLA. It works until it doesn’t. Then the scramble to understand what broke, and why, and what to do about it, begins.

The Accumulating Drift. A model was calibrated on eighteen months of historical ERP data. That calibration is now two years old. The business has changed: new suppliers, new SKUs, different process patterns. The model’s predictions are getting subtly less accurate. No monitoring exists to detect this. Nobody knows the debt is accumulating. It shows up in the next quarter-end reconciliation.

Why You Can’t Average Your Way Out of This

Something that gets missed in most enterprise AI governance discussions: not all of these deficits can be traded against each other.

Some failures are not just a dial. They are a gate.

If an AI integration that drives financial decisions has no named accountable owner, no audit trail, no rollback path, and no human review checkpoint, that is not a problem you average against clean architecture elsewhere. It doesn’t matter that your data pipelines are well governed. It doesn’t matter that your deployment automation is mature. Those things are real and valuable, but they don’t offset an unaudited, irreversible action in a high-stakes workflow.

I’ve deliberately designed the framework I’m developing around a dimensional profile rather than a composite score, and this is exactly why. An enterprise Gen-AI readiness index can do this kind of averaging: a weak risk-and-compliance score gets blended against a strong data governance score and you end up with a respectable total. That math makes no sense when the weak item is “no audit trail on an AI component that approves payment transactions.” Strong documentation doesn’t offset unbounded AI authority over financial workflows. They aren’t the same axis, and treating them as if they are is how organizations end up with a clean-looking score and a serious controls problem.

In the framework I’m developing, certain control failures trigger immediate remediation regardless of how the rest of the profile looks. No owner. No rollback. No human checkpoint on a high-consequence action. These aren’t factors to be weighed. They’re gates.

Two Costs Most Organizations Only See One Of

There are two distinct things at play here financially, and most organizations are only tracking one of them.

The debt stock is the accumulated unresolved obligation: the undocumented integration, the unpinned model version, the missing rollback path. It sits on your architecture like a balance due.

The debt interest is what you pay every day you don’t address it: the recurring validation work to check whether the model is still behaving correctly, the manual exception handling when it isn’t, the escalations when something unexpected happens, the audit preparation overhead when compliance starts asking questions about integrations nobody documented properly.

Organizations almost always see the debt interest. They call it operational friction. They call it “the team spends a lot of time dealing with AI issues.” They treat each incident as a one-off rather than as an interest payment on a structural liability they haven’t named yet.

Naming it changes what you can do about it.

This Is a actually a Leadership Problem

I want to be honest about something here, because I’ve seen the same dynamic in organizations of every size. The teams building these integrations are not being careless. They are moving fast because that’s what they were asked to do. The debt accumulates not because of incompetence but because the framework for thinking about AI integration obligations in ERP environments doesn’t really exist yet in any usable form. Or rather, it hasn’t been articulated clearly enough to act on.

Technical debt in traditional software development became manageable once organizations developed concrete practices around it: code review standards, refactoring sprints, architecture review boards. AI Integration Debt is at roughly the same stage that general technical debt was in the early 2000s, widely experienced but not yet well-framed, and therefore not well-managed.

What’s needed is a taxonomy that names the types of debt clearly enough to actually act on, an assessment approach that organizations can apply to specific integrations without a PhD-level research program, a governance model that extends existing ERP change management rather than trying to replace it, and a clear way to decide what to fix first when everything seems equally urgent.

That’s what I’m working through and will be writing about next.

Why This Matters Right Now

The first wave of enterprise AI integrations is maturing. The integrations built in 2023 and 2024 as pilots and proofs of concept are becoming load-bearing. They’re moving from the innovation budget to the operations budget. And as they do, the debt they carry moves with them.

A systematic review published earlier this year looked at 183 academic publications on AI-powered ERP systems. Governance, trust, and long-term organizational effects appeared in fewer than 2% of the literature. Automation, predictive analytics, and generative AI themes dominated everything else. The research community is studying AI adoption in ERP at enormous scale. Almost nobody is studying the accumulated governance liability that adoption leaves behind.

That gap is where AI Integration Debt lives. And based on every conversation I’m having with people running ERP environments right now, it is filling up faster than organizations realize.

Organizations that get ahead of this now will have real advantages: lower maintenance costs, higher reliability, faster ability to adopt whatever AI capabilities come next, and audit trails that hold up when compliance asks the inevitable questions.

Organizations that wait will spend the next decade managing obligations they didn’t know they were taking on.

The Point This Post Is Trying to Make

AI is not optional for enterprise ERP environments. The efficiency gains are real. The competitive pressure is real. The technology is mature enough to deliver value at scale.

But moving fast without a proper framework is not actually moving fast. It’s borrowing against the future, and in enterprise systems, the future arrives with an audit.

So let’s face it, AI Integration Debt is real. With a little focus and effort, it’s assessable at the level where it actually lives: not the enterprise, not the platform, but the specific AI component embedded in the specific ERP process.

The first step is accepting the debt and learning to see it at that level.

If this resonates with something you’re seeing in your own environment, I’d genuinely like to hear about it in the comments.

I've spent 20 years inside enterprise ERP systems. I'm now working at the intersection of AI engineering and legacy infrastructure, and writing about what that actually looks like from the inside. I'm building a research-grounded framework for AI Integration Debt and developing it through both academic research and real-world implementation experience. The goal is something practitioners can actually use, not just read about.

Plenty more to unpack here. Next I'll get into the five dimensions in detail, the assessment approach, and what the governance response actually looks like in practice.